The SK Hynix Anomaly and the Shifting ‘Korea Discount’

South Korea’s economic trajectory—rising from the devastation of the Korean War to becoming the indispensable backbone of the 21st-century AI infrastructure—is one of modern history’s most remarkable feats. At the center of this transformation is SK Hynix. Far from just a memory chip manufacturer, the company serves as the ultimate proxy for understanding South Korean corporate resilience, the glaring valuation discrepancy against global peers like TSMC, and the shifting geopolitical dynamics of the peninsula.

The Chaebol Ecosystem: From Near-Bankruptcy to AI Dominance

To understand SK Hynix, one must understand the unique “Chaebol” (family-run conglomerate) structure that acts as the safety net for South Korean industrial expansion.

The company’s history is a testament to extreme volatility and resilience:

1983: Founded as Hyundai Electronics.

2001–2010: Rebranded as Hynix in 2001, the company entered a grueling debt workout program following severe financial distress.

December 2003: Stock prices hit a rock-bottom low of just 5,000 KRW.

2012: The pivotal turning point. SK Telecom acquired Hynix.

Crucially, this was achieved without direct reliance on the SK holding company; rather, SK Telecom and SK Innovation—undisputed market leaders in the telecommunications and energy sectors respectively—served as massive cash cows to finance the acquisition and subsequent capital expenditures.

By 2026, the stock has amplified nearly 400 times from its 2003 lows. This growth is heavily insulated by its position within South Korea’s “Big 5.” According to the May 1, 2026 Fair Trade Commission (FTC) official rankings:

This conglomerate structure allowed SK Hynix to make aggressive, counter-cyclical investments during industry downturns—a luxury pure-play Western semiconductor companies rarely possess.

The Valuation Paradox: SK Hynix vs. TSMC

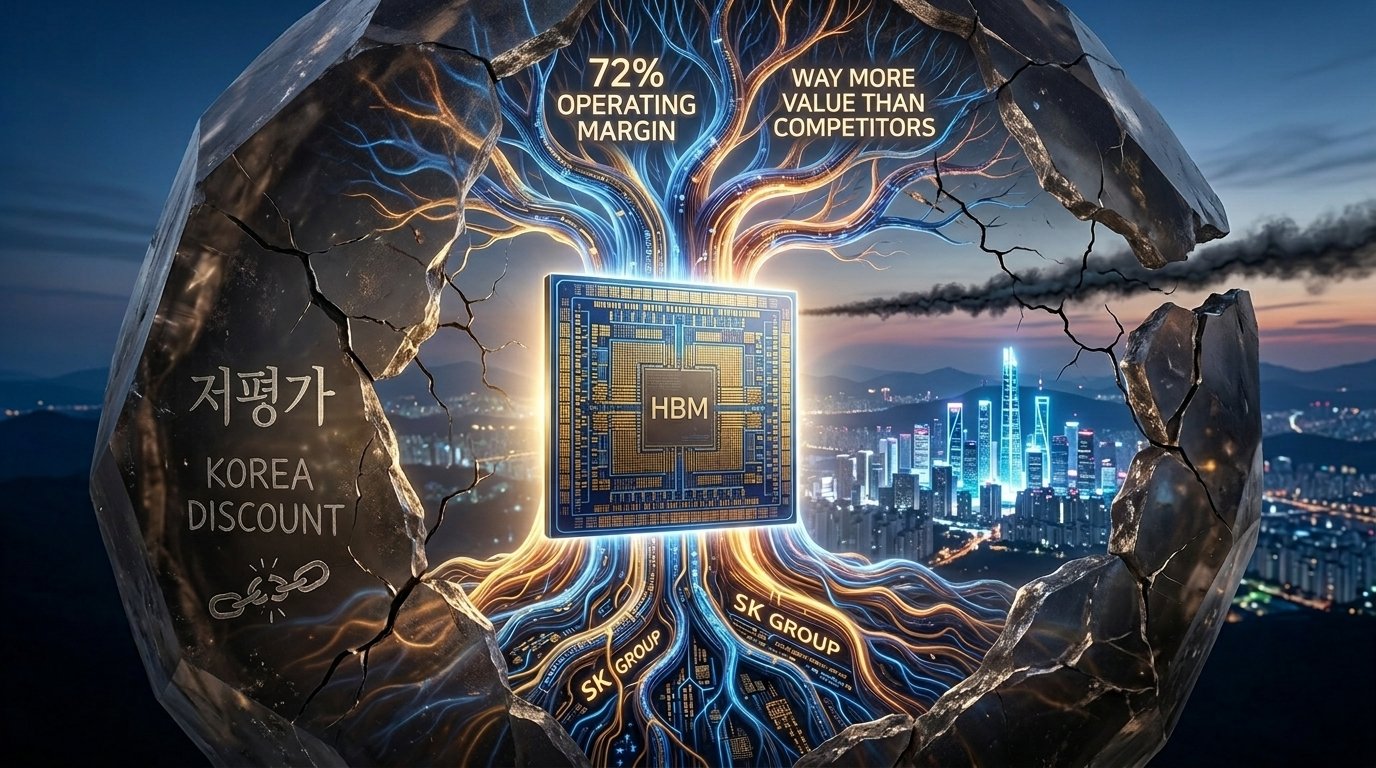

Entering 2026, SK Hynix’s operational reality radically diverges from its market valuation. Driven by a near-monopoly (roughly 59% market share) in High Bandwidth Memory (HBM) for AI accelerators, the company achieved a staggering 72% operating margin in the first quarter of 2026. This decisively outpaces global titans, including Nvidia (65%) and the premier foundry TSMC (58.1%). Furthermore, in 2025, SK Hynix posted an annual operating profit of 47.2 trillion KRW, officially beating Samsung Electronics for the first time.

Despite superior profitability, the stock remains chained by a severe valuation gap:

– Low PBR (Price-to-Book Ratio): The stock frequently trades at a discounted book value compared to its U.S. and Taiwanese counterparts, meaning the market structurally undervalues its hard assets and cash generation.

– P/E Divergence: While TSMC commands a Price-to-Earnings (P/E) ratio exceeding 30x, SK Hynix has recently hovered around the 12.5x mark.

SK Hynix possesses arguably more intrinsic value than TSMC in the current AI supercycle. While TSMC is the undisputed king of logic foundries, SK Hynix’s long-term, advance-order HBM contracts have effectively transformed its memory business into a highly predictable, high-margin, foundry-like model. Yet, the broader market often continues to price it as a cyclical commodity manufacturer.

Geopolitics and the Shifting Paradigm

The root of this valuation paradox is the infamous “Korea Discount.” For decades, foreign capital has applied a severe risk premium to South Korean equities due to intrinsic negativities: structurally rigid corporate governance and the perpetual geopolitical threat posed by North Korea. The specter of conflict has historically acted as a ceiling on the stock market.

However, in 2026, this paradigm is shifting. The current political administration is actively dismantling these barriers through aggressive reforms, notably the “Corporate Value-up Program,” which enforces stringent shareholder return mandates and capital efficiency improvements.

Simultaneously, the nature of the North Korea risk is evolving in the eyes of global investors. As the AI supply chain becomes the most critical infrastructure of the 21st century, the indispensability of SK Hynix means the company is increasingly viewed as “too critical to fail,” enjoying implicit strategic backing from U.S. and global tech interests. The geopolitical risk is slowly being priced out by the sheer gravitational pull of global AI demand, positioning SK Hynix not just as a national champion, but as one of the most compelling value anomalies in the global semiconductor landscape.