The Anatomy of a Transaction: Decoding Hidden Fees in SWIFT vs. Crypto Rails

Last Updated: June 12, 2026 by SK Pulse Editorial Team

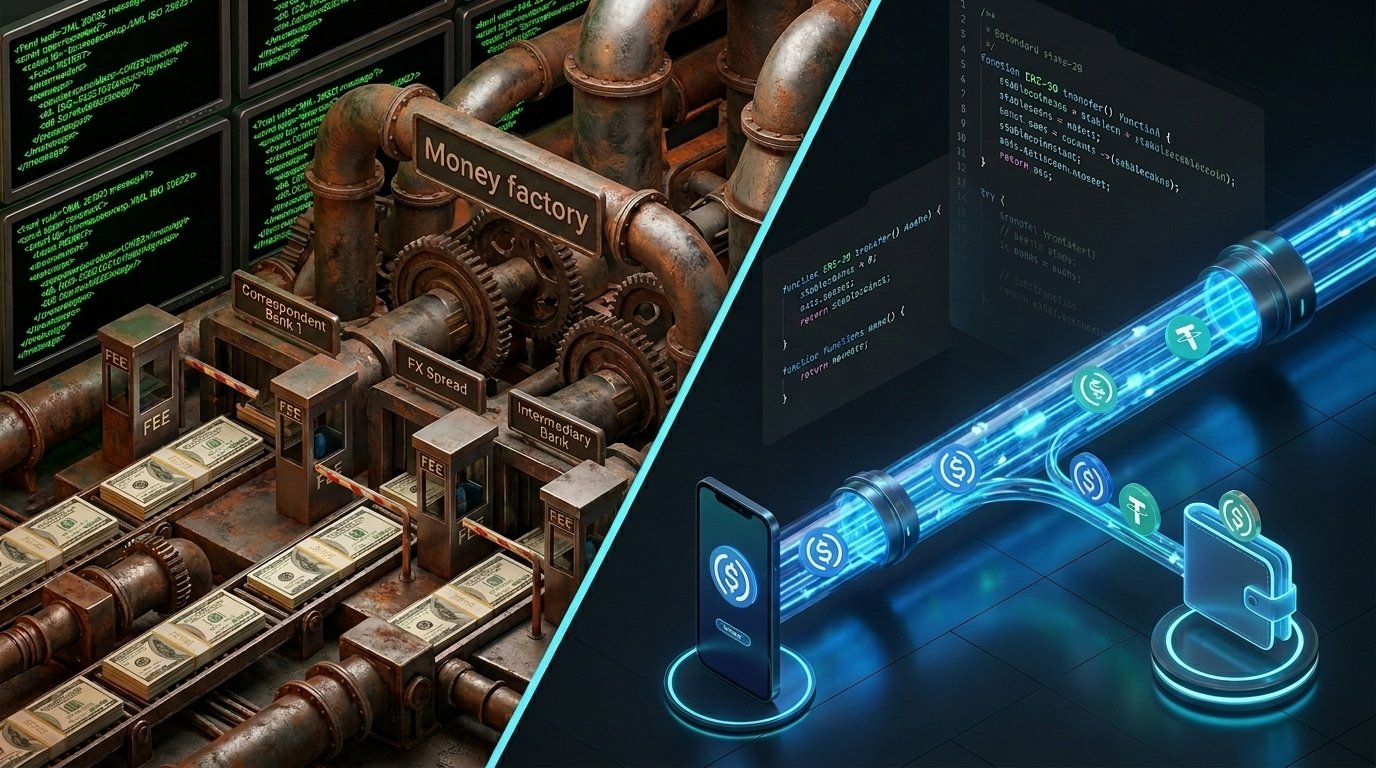

When a user taps a button on an app, money seems to teleport. But behind that seamless frontend lies a complex maze of payment infrastructure, routing protocols, and heavily monetized API calls.

For the borderless S-Corp founder running a distributed team across Asia and the U.S., understanding this infrastructure is not just a technical curiosity—it is a fiduciary necessity. In the modern financial tech stack, transactions generally fall into two categories: fee-free and fee-involved.

True “fee-free” transactions are surprisingly rare and largely limited to closed-loop systems (e.g., a standard fiat deposit within a single domestic banking ledger via ACH). But the moment money leaves its native ecosystem—whether hitting a cross-border payment gateway or executing a smart contract—friction occurs.

Let’s break down the architecture of the four types of fee-involved transactions, comparing legacy financial routing against modern cryptographic rails.

1. The Direct Crypto Loop: Fiat A ➔ Crypto ➔ Fiat A

This is the simplest on-ramp and off-ramp model, primarily enabled by heavily regulated centralized exchanges (CEXs) like Coinbase or Kraken that maintain direct banking licenses.

- The Architecture: A user pushes fiat to the exchange, executes a trade, and eventually withdraws the fiat back to their bank. Operationally, this involves stitching together a fiat on-ramp with an exchange’s execution engine.

- Where Fees Occur: Friction is exacted at every single gateway. You pay a deposit fee (or spread), a maker/taker fee to the exchange’s matching engine, another trading fee when selling, and finally, a withdrawal fee to push the fiat back through the traditional banking layer.

2. The Multi-Hop Exchange: Fiat A ➔ Stablecoin ➔ Crypto ➔ Stablecoin ➔ Fiat A

This is the most common transaction flow for advanced global traders, especially on exchanges that lack direct fiat liquidity pairs for localized geographic regions.

- The Architecture: Stablecoins (USD-pegged digital money like USDC or USDT) act as the bridging layer. Execution here requires multi-leg routing, navigating API rate limits across different pairs, and managing real-time slippage tolerance.

- Where Fees Occur: Costs compound heavily here. Users pay to convert fiat into a stablecoin, pay exchange fees to trade the stablecoin for the target crypto, pay again to trade back to a stablecoin, and pay a final fee to off-ramp. Each step triggers an exchange fee, network gas, or liquidity spread.

3. The Blockchain Remittance: Fiat A ➔ Stablecoin ➔ Stablecoin ➔ Fiat B

Widely known as the “SWIFT Killer,” this flow leverages the blockchain as a global settlement layer to bypass correspondent banking entirely.

- The Architecture: Instead of routing API calls to a centralized clearinghouse, the backend executes smart contract functions directly on-chain. A sender buys a stablecoin, pushes it across a blockchain to a foreign wallet, and the recipient cashes out locally via a P2P market or local exchange.

- Where Fees Occur: You pay three distinct fees: an on-ramp conversion fee, a network transfer fee, and an off-ramp conversion fee. However, by routing through low-cost Layer-2s or high-throughput chains like Solana, the aggregate cost becomes mathematically predictable and substantially cheaper than legacy wires.

4. The Legacy Behemoth: Fiat A ➔ SWIFT ➔ Fiat B

This is the traditional, decades-old international wire transfer. What many founders don’t realize until they review their corporate ledger is that SWIFT is not a settlement network; it is purely a messaging protocol. (This structural inefficiency is frequently highlighted in reports by entities like the Bank for International Settlements (BIS))

- The Architecture: Money doesn’t actually “move.” Instead, SWIFT sends encrypted messages between a daisy-chain of correspondent banks updating Nostro and Vostro ledgers.

- Where Fees Occur: SWIFT transactions are notorious for the opaque “four-headed fee monster”:

- Sender’s Bank Fee: An upfront charge to initiate the wire.

- The Spread: A hidden FX markup applied when converting Fiat A to Fiat B.

- Intermediary Bank Fees: Because the message hops between multiple correspondent banks, each middleman takes an unpredictable cut.

- Recipient Bank Fee: A final charge levied by the receiving institution.

The Verdict & How to Verify the Math

The transition from legacy SWIFT to blockchain rails represents a shift from routing money through fragmented geographical jurisdictions to routing it through unified cryptographic ledgers. While stablecoin remittance (Type 3) introduces multiple conversion steps, the elimination of unpredictable intermediary banks and opaque FX spreads makes it vastly superior for funding global operations.

However, relying on assumptions is dangerous for any corporate treasury. If you are managing global payroll, paying foreign contractors, or building cross-border routing logic, you must run the numbers.

To eliminate the guesswork, we built the Stablecoin vs. SWIFT Payout Calculator.

- Methodology: This tool dynamically compares the hidden spreads, intermediary cuts, and estimated transfer speeds of traditional SWIFT wires against the on-chain gas and conversion fees of stablecoin routing. Input your transfer volume to reveal the exact, data-driven cost difference.

Launch the Crypto vs. SWIFT Fee Calculator Here (Interactive Calculator)

About the Author & Editorial Policy

SK Pulse Editorial is operated by practitioners with extensive experience in international IP compliance, corporate structuring, and cross-border business operations. Our tools and analysis are designed to provide practitioner-grade intelligence for global founders, S-Corp operators, and expats navigating complex international systems.

Disclaimer: This article constitutes editorial analysis and is for informational and educational purposes only. It does not constitute financial, legal, or investment advice. The macroeconomic landscape, banking fees, and digital asset markets are highly volatile. Always consult a qualified professional fiduciary before making capital allocation or international transfer decisions.