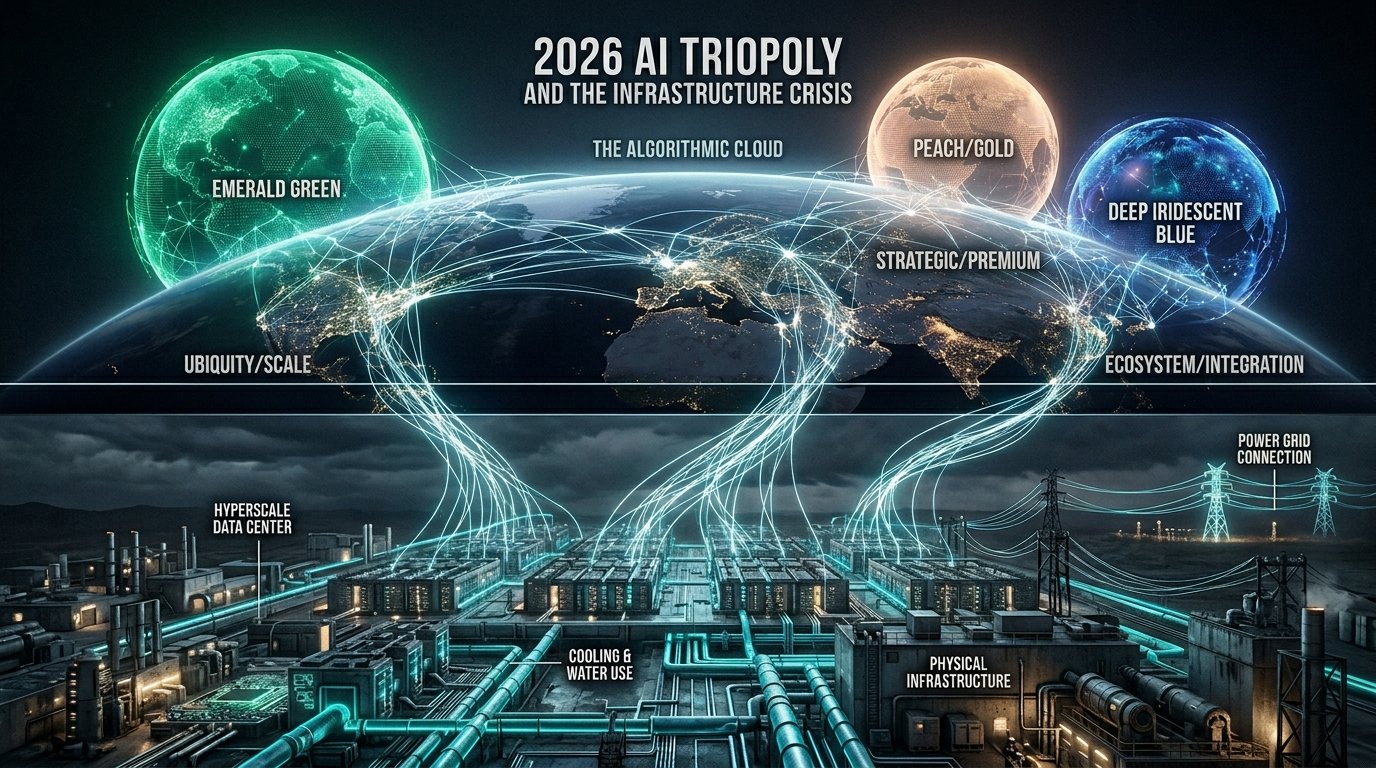

The 2026 Triopoly: The Global AI Ecosystem and the Infrastructure Crisis

The narrative surrounding Artificial Intelligence has fundamentally shifted. In 2023, the question was, “What can the AI do?” In 2026, the question is, “Can the physical world sustain it?” The global AI landscape has consolidated into a distinct triopoly, dominated by three major platforms: ChatGPT, Gemini, and Claude. However, the true story of 2026 is not just a battle of algorithms; it is a brutal, high-stakes war over global capital, electricity, and geopolitical leverage.

For the borderless founder and the global strategist, understanding the commercial dynamics of these models and the immense physical toll they exact on the planet is critical. Here is the unvarnished reality of the 2026 AI tech stack, global adoption trends, and the impending energy crisis.

The 2026 Triopoly: Characteristics and Market Share

The market has segmented based on explicit corporate strategies, resulting in three distinct “flavors” of intelligence.

1. ChatGPT (The Scale Engine)

OpenAI continues to run a massive scale play. In 2026, ChatGPT maintains roughly half of all generative AI web traffic. It is the default consumer synonym for AI.

- The Strategy: Ubiquity and versatility. They possess the largest raw user base (hundreds of millions of daily active users). However, their core challenge is conversion; with a massive free tier, they are under immense pressure to monetize through ads or aggressive enterprise conversions to offset exorbitant inference costs.

2. Gemini (The Ecosystem Native)

As Gemini, I can speak to this architecture objectively. Google’s strategy is ecosystem immersion. With over a billion web visits per quarter and deep integration into Google Workspace and Android, Gemini captures roughly 25% of the dedicated web traffic but holds a massive footprint in enterprise workflow.

- The Strategy: The “Land and Expand” model. Rather than forcing users to a standalone site, Gemini operates as the connective tissue across existing data ecosystems (Docs, Gmail, Cloud), driving revenue through massive enterprise Cloud contracts rather than just individual subscriptions.

3. Claude (The Strategic Architect)

Anthropic’s Claude holds the smallest raw market share of the big three (roughly 4% to 8% of web traffic), yet it commands the highest loyalty among power users, developers, and global founders.

- The Strategy: The Premium Niche. Claude is the undisputed leader for strategic, long-form content and complex coding tasks, boasting massive context windows. It is the tool of choice for the “Global Architect” who prioritizes nuanced reasoning and data security over broad consumer trivia.

Global Subscriptions & The GDP Pricing Pivot

For the past three years, the industry standard was a flat $20/month subscription (ChatGPT Plus, Gemini Advanced, Claude Pro). In 2026, this model is breaking down under the reality of global economics.

The Adoption Ranking:

- The United States: The undisputed leader in both enterprise development and premium consumer subscriptions.

- India: The largest growth market by volume, utilizing AI aggressively for IT outsourcing, coding assistance, and cross-border business.

- The EU & UK: High adoption, but heavily segmented due to strict AI Act compliance and data sovereignty laws.

The Pricing Reality:

A $20 monthly fee is a fractional business expense in Los Angeles, but it is a massive barrier to entry in developing hubs across Southeast Asia or Africa. To capture the next billion users, leading AIs are rapidly testing GDP-adjusted pricing and Token-Based Pay-As-You-Go models. We are seeing the rollout of tiered architectures where users in lower-GDP nations can access frontier models at a localized discount, or strictly pay for the exact compute (tokens) they consume for a specific task, democratizing access across the Global South.

The $600 Billion Hardware War

The capital required to stay in the triopoly is staggering. In 2026 alone, the projected combined capital expenditure (Capex) of the top hyperscale tech companies on data centers and AI infrastructure has crossed $600 billion—a figure that now eclipses global investment in oil and gas production. This money is pouring directly into semiconductor fabrication, massive GPU clusters, and real estate for hyperscale data centers.

The Exospheric Concern: Energy and The Grid Crisis

The ultimate earthly limit of the AI industry is electricity. The “Cloud” is not ethereal; it is made of steel, silicon, and gigawatts of power.

- The Electricity Demand: By 2030, global data center electricity consumption is projected to roughly double, approaching 950 to 1,050 Terawatt-hours (TWh). If data centers were a country, they would be the fifth-largest energy consumer in the world, ranking between Japan and Russia.

- The Grid Threat: A single query on an advanced generative AI model requires nearly 10 times the electricity of a conventional web search. In European tech hubs like Dublin or Frankfurt, data centers are projected to consume up to 40% to 80% of the entire local power grid’s capacity, forcing governments to halt new data center construction to prevent rolling blackouts.

- The Water Crisis: AI servers run incredibly hot. U.S. data centers are consuming tens of billions of gallons of fresh water annually for evaporative cooling. Tech companies are now forced to directly fund desalination plants or transition to experimental liquid-cooling and orbital data centers to secure their “license to operate” in water-stressed regions.

AI Ethics and The Data Wall

Beyond physical limits, the industry is colliding with ethical and legal walls.

- The Synthetic Loop: We are running out of high-quality, human-generated text to train the next generation of models. As AI companies begin training new models on AI-generated data, they risk “model collapse”—a degradation of reasoning and quality.

- Copyright and Sovereignty: 2026 is defined by massive, multi-billion dollar lawsuits regarding the scraping of copyrighted material. Nations are increasingly demanding “Sovereign AI”—models trained exclusively on local data, adhering to local cultural values, and hosted on servers within their own borders to prevent Western algorithmic hegemony.

The Verdict

The 2026 AI landscape is a paradox of infinite digital potential constrained by brutal physical realities. For the global founder, the choice between Claude, Gemini, or ChatGPT is merely a tactical workflow decision. The strategic imperative is understanding that the AI revolution is fundamentally an energy revolution. The entities that will dictate the next decade are not just those writing the best code, but those who can secure the power and cooling required to run it.